Pallab Bhattacharyya

Pallab Bhattacharyya

The relentless churn of global conflicts—the US-Israel-Iran war, the Israel-Lebanon tensions, the protracted Russia-Ukraine confrontation, and associated disruptions—has exposed the fragility of the world’s hydrocarbon and fertiliser supply chains. These overlapping crises have sent shockwaves through oil, natural gas, and fertiliser markets, driving prices to volatile highs and threatening energy security and food production worldwide.

With the Strait of Hormuz carrying roughly one-third of global fertiliser shipments and a significant share of oil and LNG, even localised tensions in the Gulf have triggered sharp spikes: urea prices surged by up to 49%, Brent crude reached $110 per barrel, and gas futures in Europe jumped dramatically. For import-dependent nations, the consequences ripple far beyond economics, raising food costs, squeezing farm margins, and underscoring the urgent need for diversified, resilient alternatives.

In this crucible, biofuels, renewable gases, green hydrogen, and low-carbon fertilisers have shifted from niche environmental tools to strategic imperatives for energy sovereignty and climate resilience. India, with its vast agricultural diversity, abundant solar and wind resources, and policy momentum, stands uniquely positioned to lead this transformation while turning crisis into opportunity.

The geopolitical shocks of recent years have laid bare the structural vulnerabilities of fossil-dependent systems. Russia’s role as a major oil and gas exporter meant that sanctions and disrupted flows after its 2022 invasion of Ukraine caused Brent and WTI (West Texas Intermediate) prices to spike above $130–140 per barrel, while European gas supplies plummeted by around 80%, forcing a scramble for LNG and tightening global markets. More recently, instability around Iran and the Strait of Hormuz has compounded these pressures, disrupting not only energy but also fertiliser routes from key Gulf producers like Qatar, UAE, and Iran itself—a major urea exporter.

India, one of the world’s largest urea consumers, imports a good part of its fertiliser needs and relies heavily on imported natural gas for domestic production, making roughly 20–25% of its supply chain exposed to these chokepoints. The absence of strategic fertiliser stockpiles akin to petroleum reserves amplifies the risk, potentially depressing application rates and jeopardising food security for 1.5 billion people. Yet, these very disruptions are catalysing a paradigm shift toward locally sourced, environment-friendly options that decouple economies from volatile foreign supplies.

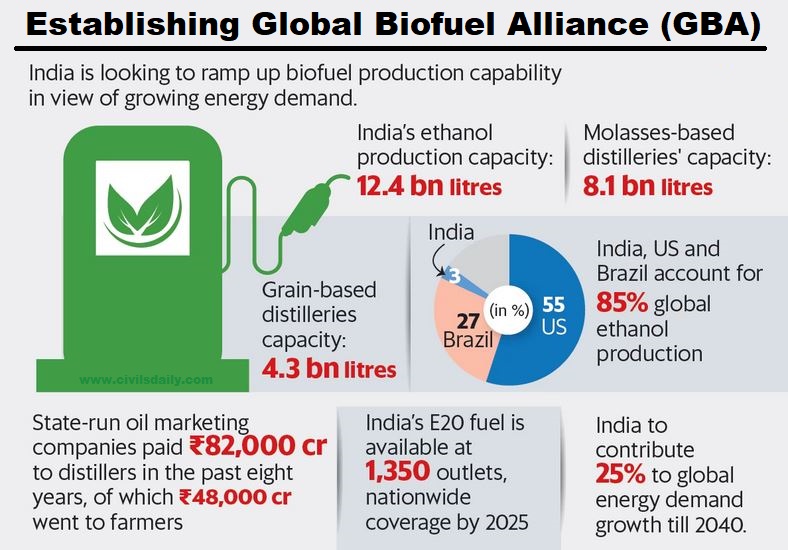

Biofuels have emerged as a cornerstone of this response, offering “drop-in” replacements for petroleum fuels with significantly lower lifecycle greenhouse gas emissions—often 50–80% less when produced sustainably. Global liquid biofuel production has grown by about 50% over the past decade, led by the United States (primarily corn ethanol) and Brazil (sugarcane ethanol and soy biodiesel), which together account for roughly two-thirds of output. Brazil, in particular, derives around 22% of its transport energy from biofuels, supported by long-standing blending mandates, tax incentives, and flex-fuel infrastructure—a model born from the 1970s oil crises that has saved billions in imports and avoided vast emissions.

The United States reinforces this through its Renewable Fuel Standard, which sets ambitious volume obligations and promotes advanced biofuels through credits, and through the Inflation Reduction Act.

India spends nearly ₹22 lakh crore every year on fuel imports, with 87% of its energy needs dependent on foreign sources. @nitin_gadkari’s strong push for alternative fuels is the bold shift the nation needs right now.

— CM ReportCard India (@CMReportCard_) April 25, 2026

This is not just an energy reform, it is the real road… pic.twitter.com/QBvdH7AngG

Nordic countries like Sweden, Finland, and Denmark have integrated bioenergy to exceed 20% of primary energy supply, complementing renewables with rigorous sustainability criteria that cap food-based fuels and prioritise waste and residues. Even China and other emerging players have accelerated production, with double-digit growth in recent years through incentives for biodiesel and waste-oil feedstocks. These experiences demonstrate that stable mandates, infrastructure investment, and farmer engagement can embed biofuels deeply into national systems, enhancing energy security while mitigating climate impacts.

India has moved decisively in this direction, leveraging its policy architecture to accelerate the transition. The National Policy on Biofuels (2018), updated in 2022, advanced the 20% ethanol blending target (E20) to 2025–26, expanding eligible feedstocks to include molasses, sugarcane juice, damaged grains, and non-edible oils. Blending rates have climbed steadily, reaching nearly 20% in mid-2025, delivering substantial foreign exchange savings and additional income to sugarcane and grain farmers.

Complementary initiatives like the SATAT (Sustainable Alternative Towards Affordable Transportation) scheme promote compressed biogas (CBG) from agricultural residues, cattle dung, and municipal waste, with offtake guarantees from oil marketing companies. This not only displaces imported natural gas but also tackles stubble burning, air pollution, and waste management—turning rural liabilities into assets.

Advanced second-generation ethanol plants using crop residues are being scaled under schemes like Pradhan Mantri JI-VAN (Jaiv- VatavaranAnukoolfasalawaseshNivaran), prioritising non-food feedstocks to avoid competition with food security. India’s participation in the Global Biofuel Alliance further amplifies these efforts through international collaboration on standards and technology.

Parallel innovation in low-carbon gas and fertiliser pathways offers even deeper resilience. Conventional ammonia production, reliant on natural gas reforming, locks fertiliser prices to volatile energy markets and emits massive CO₂. Green ammonia, produced via electrolysis of water using renewable electricity to generate hydrogen, followed by synthesis with nitrogen, slashes emissions to near zero and stabilises costs through long-term power purchase agreements. India’s AM Green project at Kakinada exemplifies this frontier: a 1 million-ton-per-year green ammonia facility backed by 2.3 GW of round-the-clock renewables (wind, solar, and pumped hydro storage), with electrolyser capacity already contracted and offtake deals signed for both domestic use and export to Europe and Asia.

Graphics by SSCIS

Graphics by SSCIS

Blue ammonia captures and sequesters CO₂ from gas-based plants, providing a transitional bridge, with retrofits underway in the US and elsewhere supported by tax credits. Biogas and biomethane add another layer, produced from waste streams and upgraded for grid injection or transport, while their digestate serves as nutrient-rich bio-fertiliser, closing circular loops.

Countries worldwide are reaping gains from these shifts. Brazil’s decades-long biofuel commitment has not only buffered oil shocks but also fostered rural development. The EU’s REPowerEU plan and “Fit for 55” package, accelerated post-Ukraine, emphasise advanced biofuels, renewable fuels of non-biological origin, and carbon border adjustments to drive decarbonization globally. Morocco is emerging as a green hydrogen and ammonia exporter, leveraging solar and wind for Power-to-X projects.

In India, the National Green Hydrogen Mission targets 5 million tonnes of green hydrogen annually by 2030, with auctions and offtake agreements already linking refineries, fertiliser plants, and steel to lower-carbon pathways. Complementary efforts like PM-KUSUM solarise agricultural pumps, enabling farmers to generate and sell surplus power, while PM-PRANAM incentivises states to reduce chemical fertiliser use through grants for bio-fertilisers and organic amendments. Nano-urea and integrated nutrient management help enhance efficiency, improving soil health and yields.

This multifaceted transition aligns perfectly with India’s strengths: immense agricultural diversity for varied feedstocks, world-class renewable potential in states like Rajasthan, Gujarat, and Tamil Nadu, and a policy ecosystem that empowers farmers as both food and energy providers—“Annadata to Urjadata.” By prioritising residues and wastes for biofuels and CBG, India safeguards food security while generating rural income, creating jobs, and cutting imports.

Challenges like scaling advanced technologies, ensuring sustainability to prevent indirect land-use issues, managing costs during the green premium phase, and building infrastructure remain, but international best practices and domestic innovation provide clear pathways. Robust mandates, viability gap funding, sustainability safeguards, and public-private partnerships, as seen in Brazil and the US, can accelerate progress.

Ultimately, these geopolitical conflicts, painful as they are, serve as a powerful catalyst for humanity to embrace decentralised, environment-friendly production modes that insulate nations from localised shocks. For India, the convergence of energy security, climate goals, and rural prosperity offers a historic opportunity to pioneer a resilient, low-carbon future.

ALSO READ: Iran's unprecedented toll on Hormuz passage will impact oil prices

Through biofuels, bio-methane, green ammonia, and bio-fertilisers, the country can weather current storms and emerge stronger.

.webp "A Maulana with the ancient hand-written Quran")